•

article

What is a chargeback?

Well, to put it simply, a chargeback is a return of funds from you, the merchant, back to your customer.

However, they differ from traditional refunds because the consumer asks their bank to credit them by forcibly removing funds from your business’s bank account, rather than contacting you directly. If the bank deems the chargeback valid; your business may be subject to chargeback fees and a negative reputation.

And to a hardworking business owner, an unwanted removal of your funds along with a negative image can be detrimental to your business’s success.

Why do chargebacks exist?

Chargebacks are in the interest of the consumer; they protect them against unauthorized or fraudulent transactions. It’s the consumer’s backup plan to ensuring their money is always safe.

Nonetheless, consumers are not just protecting themselves from your run-of-the-mill criminal. Chargebacks also deter merchants from being deceitful and selling subpar products and services.

At the end of the day, customers shouldn’t have to pay for something they did not purchase themselves, for something that was not as described, or for charges that should never have been placed.

Furthermore, there are over 100 reasons why a customer could be disputing a charge. Here is a list of the most common chargeback reasons:

- Your customer did not receive said product or service

- Your customer does not recognize the charge on his/her credit card statement

- Your customer believes the product or service is not as it was described or it is defective or damaged

- Your customer’s credit card was stolen or used without consent (credit card fraud)

- Or a duplicate transaction

But how does it all work? And what are your options if you get a chargeback?

Below is a detailed breakdown of the entire chargeback process and what your role is at each step.

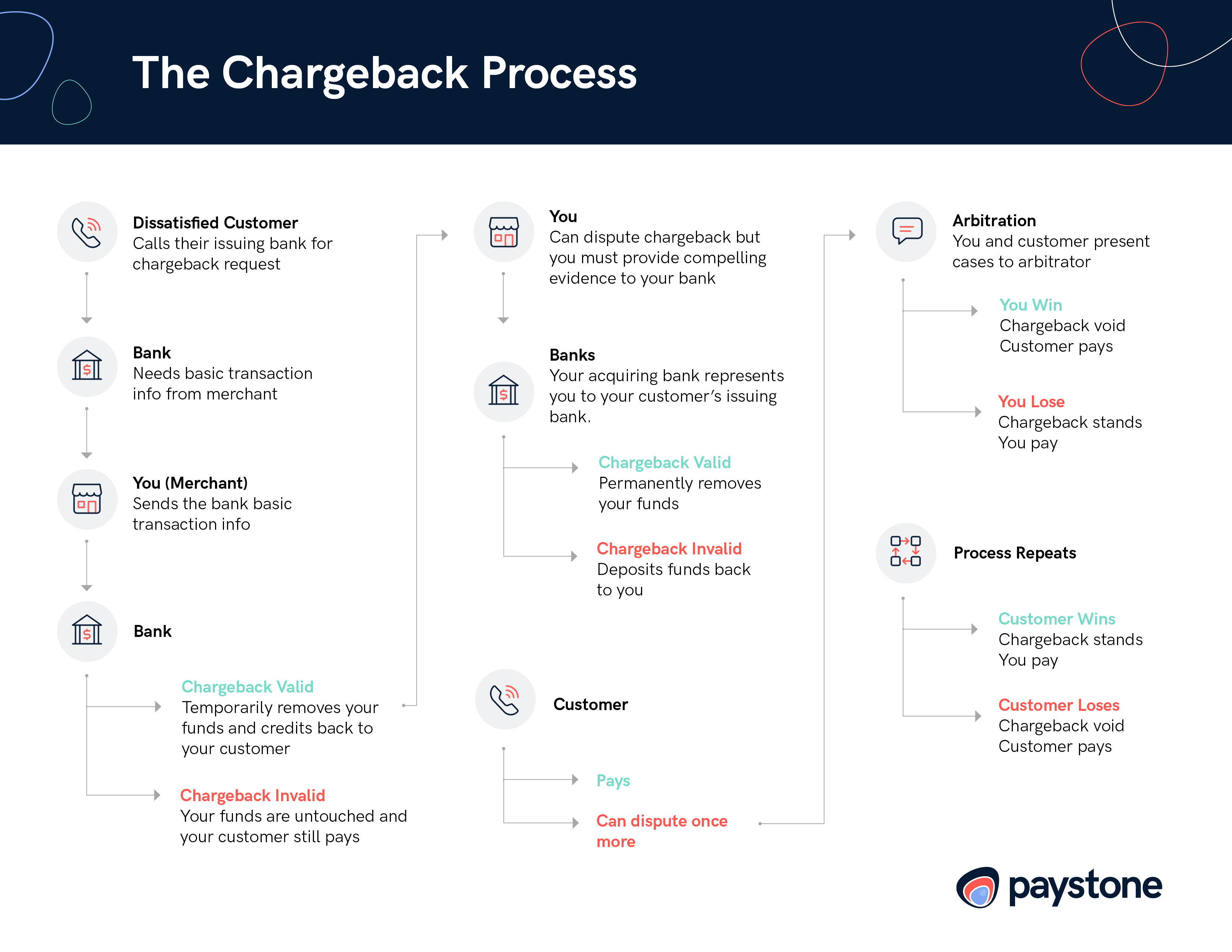

The Chargeback Process:

Your dissatisfied customer (or cardholder) contacts their issuer (the bank behind their credit card) to request a chargeback. Each chargeback reason is characterized by a reason code (or numerical value used by the card brands) and each code has its own set of rules (filing time limitations, mandatory documents, etc.).

The issuer then requests the acquirer (your bank) to contact you for basic transaction info via your payment processor. You, then, must respond within usually 10 days or failure to do so will result in your customer winning the chargeback.

Once the information has been retrieved, the issuer reviews the accuracy of the claim. If it is considered invalid or unreasonable, then the customer is still responsible for payment, your funds are untouched, and the chargeback is void.

If your customer appears to have a valid claim, the issuer will temporarily remove the funds from your bank account and credit it back to your customer. You will then be notified of the chargeback and you will likely be subject to costly chargeback fees from your acquiring bank.

As a merchant, you are entitled to chargeback rights presented to you by the card brand networks (visa, mastercard, etc.) such as being able to dispute a chargeback. If you choose to do so, your acquirer will review your case. If you are able to gather the compelling evidence needed to fight the chargeback and prove invalidity, your acquirer will act on your behalf and represent the chargeback to the issuer.

Some examples of evidence needed to represent a chargeback:

- Delivery confirmation receipt

- Proof of the original item description

- Photographs

- Proof of refund

- Proof of replacement product sent

- Signed contract or order

- Proof of return policy communicated

- Shipping verification

- Address verification

- CVV match

- Past purchase history

- Subsequent transactions from customer

- Sales receipt

- Purchaser’s IP address for eCommerce

The issuer will review the compelling evidence you and your acquirer have provided. If your evidence doesn’t successfully disprove your customer’s claim, the chargeback stands and your funds are permanently removed from your bank account.

If your evidence successfully disproves your customer’s chargeback claim, the funds will be deposited back into your account and the transaction will, again, get posted to your customer’s statement. This process can take many weeks.

In the case of you winning representment, your customer can try to request a chargeback once again and the chargeback process will repeat. You can then choose to dispute the chargeback once again or agree to arbitration.

When there doesn’t seem to be a resolution in sight, you can choose for an arbitrator to step in. You and your customer will present your cases and submit all evidence to the card brand network’s arbitrator. This is a costly but sometimes necessary last resort, as fees are usually a minimum of $300 and the process can take weeks.

And what’s worse, if you use an aggregator (like Paypal) your funds may be held throughout the entire chargeback process.

Bottom Line

Ultimately, as a business owner, you want to avoid chargebacks at all costs. When a chargeback occurs, not only are you at a loss of your product or service that was sold, but any transaction processing fees, shipping costs and sale revenue are also at a loss. On top of any chargeback fees, the stress caused from countless hours spent collecting evidence and connecting with your acquirer can be exhausting.

This lengthy chargeback process can also leave irreparable damage to your business. If you receive too many chargebacks, you could be labeled a high-risk merchant to all banks which usually means higher chargeback fees, possible fines of up to $25,000, and in certain cases, bank account closure.

It’s important to know how to prevent chargebacks and how to be ready if a chargeback occurs.