When you’re setting up your business, it can be an overwhelming process to make sure you’re not missing a critical step. One of the things you’ll definitely need is a trusted merchant services provider (like us) to make accepting payments easy.

But, even that’s not always easy. Understanding security (what the heck is PCI compliance?), fees, and above all, pricing models can be tricky.

To make things simple, we’re going to lay out the basics of flat rate pricing versus interchange plus (cost plus) pricing, and help you understand what option is the best fit for you and your business.

Flat Rate vs. Interchange Plus (Cost Plus) Pricing:

Flat Rate Pricing

What is it?

Flat rate pricing is when you pay the same processing cost for every credit card transaction, regardless of the different interchange rates for different credit card types (debit cards are charged a small per transaction fee).

What do you pay?

You pay a fixed percentage on each transaction, plus a per transaction fee.

Example: If you made $100 and did 5 transactions, here’s what you would pay.

2.6% + 5 cents per transaction

= $100 x 2.6% + $0.05 x 5 transactions

= $2.60 + $0.25

= $2.85

Benefits

- Super simple to understand

- No fluctuation in interchange rates (but you might see a slight difference in the rate if you’re accepting payments through virtual terminals versus in-store with EMV chip)*

*Interchange rates are higher for card-not-present transactions (virtual terminal, eCommerce, mail and telephone) because of the higher risk for credit card fraud.

Drawbacks

- Depending on the card type most frequently processed, it can be a more expensive option than Cost Plus

Who is it best for?

- Small businesses and start-ups processing less than $5,000 per month

- Businesses whose customers are mainly paying for items in-person

- Merchants who are looking for an easy-to-understand statement and payment structure

Interchange Plus (Cost Plus) Pricing

What is it?

Interchange or Cost Plus pricing is when your interchange percentage rate differs based on the card brand and card type used. For instance, Visa or Mastercard charge different interchange rates based on card brand and tier of card used (premium rewards cards have a higher rate than a basic credit card with no rewards).

What do you pay?

You pay different rates for the different cards and card brands used, as well as the markup for the processor’s services. Since the interchange rate depends on the card brand and type used, you might see 10 different percentages on your bill.

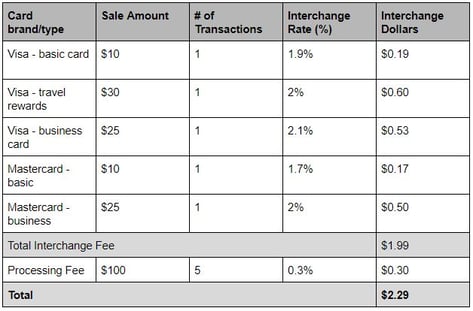

Example: If you made $100 over 5 different transactions, with customers using 6 different card brands and types, your bill might look something like this.

Benefits

- Often a less expensive option than flat rate pricing

- If interchange rates decrease, your business automatically benefits

- It’s transparent. You can see a breakdown of all the different interchange rates

- Typically no hidden fees

Drawbacks

- Way more complicated to understand

- Interchange rates are set by the card brand companies, and they are subject to change 2x per year

- Different interchange rates for different cards can make it difficult to forecast net revenue

Who is it best for?

- Medium-large businesses processing more than $5,000 per year

- Businesses whose customers are making purchases in-person, online, or through virtual terminals

- Merchants who want to see a breakdown of all the fees and different rates

Still not sure which pricing model is best for you? We can help you find the right fit for your business.

But first, why not check out some smart terminals with features to help streamline your business?